A car accident can be overwhelming, but taking the right steps afterward is crucial for securing compensation for repairs and medical bills. Filing a claim may feel daunting, especially while recovering, but a well-documented and timely claim can help prevent financial loss.

A Step-by-Step Guide to Filing a Claim

The success of your claim often depends on the groundwork you lay before you even dial your insurance company’s number. By following a structured approach, you can ensure nothing slips through the cracks.

1. Gathering Information at the Scene

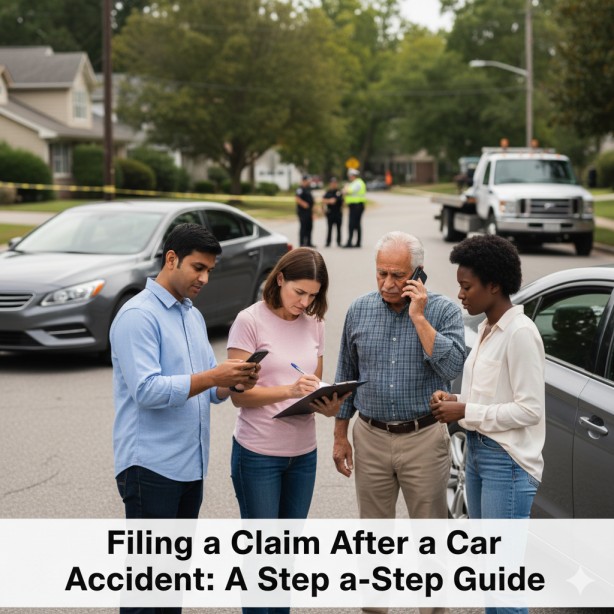

The claims process actually begins the moment the accident occurs. While your priority is always safety and medical attention, gathering evidence at the scene is vital for establishing facts later. If you are physically able to do so, try to collect as much information as possible before leaving the site of the crash.

First, exchange crucial details with the other driver. You will need their full name, contact information, insurance company name, policy number, and driver’s license number. It is also helpful to note the make, model, and color of their vehicle, along with the license plate number.

Next, turn your attention to the environment. Use your smartphone to take photos of the scene from multiple angles. Capture the damage to both vehicles, skid marks on the road, traffic signs, and weather conditions. These photos can serve as undeniable proof if there is a dispute about how the accident happened.

Finally, look for witnesses. If anyone stopped to help or saw the collision occur, ask for their names and phone numbers. A neutral third-party statement carries significant weight with insurance adjusters who are trying to determine fault.

2. Notifying Your Insurance Company

Once you are safe and have left the scene, your next step is to contact your insurance provider. Most policies have a clause requiring you to report accidents “promptly,” though the specific timeframe can vary. Delaying this notification can give the insurer grounds to deny your claim.

When you call, stick to the facts. Provide the date, time, and location of the accident, along with the information you gathered from the other driver. Be honest, but avoid speculating on who was at fault or the extent of your injuries until you have seen a doctor. A simple “I am visiting a doctor to get checked out” is safer than saying “I feel fine,” as some injuries, like whiplash, may not present symptoms for days.

Ask your agent specifically what forms you need to fill out and if there are deadlines for submitting additional evidence.

3. Documenting Damages and Injuries

Documentation is the currency of insurance claims. Without paper proof, your losses are theoretical in the eyes of the insurer.

Start by visiting a medical professional immediately, even if you feel okay. This creates a medical record linking any potential injuries directly to the accident. Keep copies of all medical reports, bills, prescription receipts, and discharge instructions. If you miss work due to the accident, ask your employer for a letter verifying your lost wages.

For vehicle damage, get repair estimates from reputable auto body shops. While the insurance company may ask you to visit their preferred shop, you are often entitled to your own independent estimate as well.

During this phase, you may realize the situation is more complex than a simple fender bender. If liability is contested or your injuries are severe, professional legal help might be necessary. Car accident attorneys in Provo and other regions often specialize in helping victims gather the necessary evidence to build a strong case against reluctant insurance providers.

4. Filing the Claim

With your evidence gathered and your insurer notified, you are ready to formally file the claim. This is often done through an online portal, a mobile app, or via email with an assigned claims representative.

Submit all the documentation you have collected: the police report (if one was filed), photos, witness contacts, and medical records. Ensure you keep copies of everything you send. When you submit the file, you will be assigned a claim number. Keep this number handy, as you will need it for every future interaction regarding your case.

Dealing with Insurance Adjusters

Once your claim is filed, an insurance adjuster will be assigned to your case. It is important to understand their role to navigate the conversation effectively.

Understanding the Role of the Insurance Adjuster

The insurance adjuster investigates the accident to determine how much the insurance company should pay. While they may be polite and professional, remember that they work for the insurance company, not for you. Their primary goal is to settle the claim for the lowest possible amount while fulfilling the company’s contractual obligations.

Be cautious during your conversations. Adjusters may ask you to give a recorded statement. You generally have the right to decline this until you are better prepared or have consulted with a legal professional. Stick strictly to the facts you have already documented and avoid offering personal opinions or emotional commentary.

Negotiating a Settlement

It is common for the adjuster’s first settlement offer to be lower than what you actually need. This is a standard negotiation tactic. Do not feel pressured to accept the first number they throw out, especially if you are still undergoing medical treatment.

Review the offer against your documented expenses. If the offer doesn’t cover your medical bills, car repairs, and lost wages, reject it politely and explain why. Send a counter-demand letter outlining your total damages with the supporting evidence attached. Point to specific documents—like a doctor’s prognosis for future therapy—to justify your counter-offer.

Patience is key here. If the insurer refuses to budge and the gap between their offer and your expenses is significant, this is the stage where arbitration or legal action typically becomes necessary.

Conclusion

Filing a car accident claim is essential for financial recovery. Stay organized, gather evidence, and understand insurance adjusters’ motivations to improve your chances of a fair outcome. Know your policy, keep detailed records, and ask for clarification when needed. A clear and methodical approach will help you navigate the process and get back on the road.

{kind=link}